As AI is making its mark, revolutionizing all industries, it is time for the insurance companies to jump on the bandwagon. AI can offer several uses for the insurance industry, from simplifying claims management to enhancing customer experience. In this article, we discuss the A to Z of implementing AI in insurance companies.

Artificial Intelligence, or in short AI is taking every industry by surprise. This technology can enable machines to act like humans and make intelligent decisions. With this ability, the technology can automate redundant tasks while also handling complicated processes with higher efficiency and accuracy.

This is causing a welcome disruption in various industries as stakeholders started to realize the potential benefits of embracing Artificial Intelligence. For the same reasons, Artificial intelligence is entering the insurance industry to transform its processes.

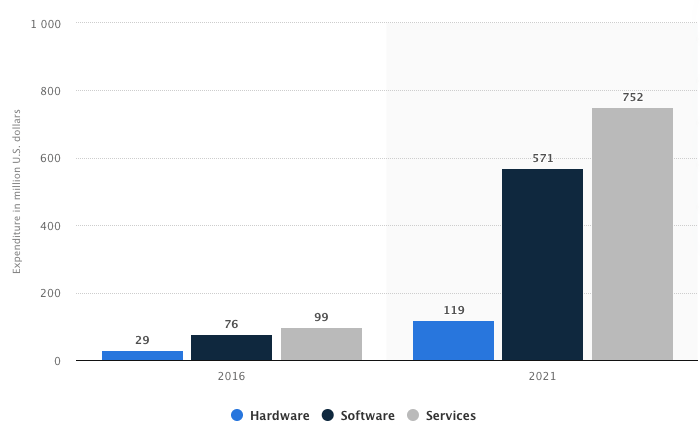

According to a study, the global insurance industry spent $76 million on software for cognitive/AI technologies, which is due to rise to $571 million by 2021.

These days, customer expectations have also been changed. One influence has been the increase in customers who now realize the value of insurance covers during a sudden advent of a deadly virus. Thus, now more than ever, the industry needs to utilize the latest technologies to catch up with the growing demands.

To know more about the scope of AI in insurance companies and how insurers can embrace AI, take a look at the below topics:

Why insurers should embrace AI?

Any insurance company is comparable to a very complex machine. Running on screws and fulcrums operating in tandem to move the system forward. The company has to exhibit outstanding performance in market analytics, market fit policy designs, seamless claims management, fail-proof risk estimation, and a hundred other critical elements that define the success of the business.

Every insurance company out there is performing all these functions. And now, the differentiator for success is defined by ‘who does it better?’ Several inherent factors limit a company’s performance. For example, a company can be limited by human power, effectiveness or efficiency of human power, limited by capital, and so on.

[contact_sales title=”Need help developing your AI project?” desc=”Reach out to us today and get started!” btn_text=”Contact Us” url=”https://accubits.com/ai-development-company/”]

Today, as the business competition is getting stiffer, those companies who can identify its limitations and frame quick solutions stand a better chance to win the market. This is where AI technology can be a savior. It can help insurers to rectify many of the limiting factors utilizing process automation. On a high-level view, AI can help insurers in four broad areas.

- Enhance operational efficiency

- Enhance insurance sales

- Enhance customer experience

- Faster and accurate market analysis

Enhance operational efficiency

Technology and innovation haven’t been the forte of the insurance industry but it is the need of the hour. Embracing AI in the insurance sector has the capacity to revolutionize the business by improving its operational efficiency and cost savings. Artificial Intelligence can optimize so many processes while providing insights that will make the organization grow. To keep up with the times and monetize on AI’s advantages, here are a few ways AI can renovate the insurance industry’s processes

- Automating claims management: End-to-end claims management processes can be automated by using AI in insurance companies. Creating settlements, capturing data or information retrieval, tracking payments and recovery, processing legal issues, authorizing and approving clients and transactions can be simplified by utilizing Artificial intelligence. One can also simplify data capture, manage communication and interaction and the software can review claims, verify policies, and process transactions. Streamlining and automating these functions is one of the main benefits AI can offer.

- Fraud prevention: Insurance fraud is a big mess, it costs billions of dollars lost annually for insurers. But today, AI models are able to predict insurance frauds based on advanced data analytics. By using machine learning technology, it is possible to interpret transaction data to discover patterns that can help detect fraud. AI-powered fraud prevention systems can assist human counterparts to better evaluate insurance claims and insurance applications.

Related Article: How AI can bring an automated insurance claim to reduce fraud.

- Hyper automation: Hyper Automation is one of the most trending technologies that can add a lot of value to the insurance sector. In a nutshell, it is the combination of Robotic Process Automation technology with Artificial Intelligence. This combination of technologies offers a myriad of benefits, as it enables machines to have the intelligence to automate more complicated tasks. A few examples for the functions that can be automated are pointed below;

- Automate insurance underwriting – A big part of the underwriting process consists of data collection and data processing. Using RPA technology, we can automate the process of data collection from various sources and data processing, resulting in faster execution of the underwriting process. RPA tools can also be configured to fill multiple fields in the internal form with relevant information and generate reports for assessing the loss of runs and thereby automating the underwriting and product pricing processes.

- Damage assessment: AI can assess the damage that occurred in accidents and implement claims accordingly. AI can analyze the photographs of incidents with help of computer vision and can measure the damage using the proper metrics and dataset. With this feature, we could eliminate biased decision-making.

Related article on Automating vehicle damage estimation using AI

Enhancing insurance sales

AI provides a wide range of opportunities for insurance companies to enhance their market penetration and product sales. The traditional method of business development is being overthrown by data-driven methods across all industries. And this trend is most critical for the insurance sector as well. The companies already hold humongous historical data that can be used to train AI models to enhance product sales.

Such AI systems can consider a wide range of signals such as customer geography, demographics, buying power, etc to generate actionable insights that can help the company to make informed decisions on sales and marketing initiatives. AI systems can also be utilized to provide customized advice and sell products that are appropriate and relevant to them.

Enhancing customer experience

AI has the potential to enhance customer interactions by automating them and providing a personalized experience. Chatbots can grab a customer’s social and geographic data providing a smooth buying experience. On-demand insurance can also be automated as carriers can let customers tailor coverage based on certain events or products. Chatbots can be present 24*7 to answer the customer’s questions and ease up the load on employees by solving basic policy-related problems and handling issues and grievances.

- Conversational tools: Before buying any product, customers do research about it. The same applies to insurance products as well. But today, the turnaround time for a customer to get the relevant information would be hours, if not days. This is because insurance agents need to deal with a large volume of prospects, making it hard to attend to everyone’s queries on time. But this need not be a pain point as today, AI-powered conversational tools like AI-chatbots can deliver accurate and relevant information to customers instantaneously. The chat program can be customized to do complex functions like calculating the premium amounts, responding with personalized product information, and much more.

- Customized products: Today, one size fits all concept is not working out very well and customers demand more personalized services and products. They would be more interested in a tailor-made insurance product rather than a broad insurance package. AI models can help insurers to create personalized insurance products specific to a user persona or even a specific individual, by incorporating various parameters like risk factors, buying power, historical data, etc to formulate an insurance plan and premium details.

- Rewards and cash-backs: AI-enabled insurance systems can systematically provide rewards and cashback to the customer. The AI can analyze the dataset by tracking the status of each customer and evaluate the reward metrics by following up on their payments. AI can allot the offers according to the insurance packages and create a reward strategy to attract users for better insurance packages and services.

Accurate market and risk analysis

- Regulatory compliance: The landscape of insurance regulations is fast-changing, and the number of insurance regulations in existence is reaching overwhelming levels, with different regions and regulators publishing policies more frequently. And this makes it harder for regulatory change management professionals, as they have to manually analyze a large number of online documents each day to identify the regulatory, policy, and procedure changes that apply to their organization.

This task is highly monotonous, tedious, and highly prone to human errors. Major insights could be overlooked if data is not organized, indexed, and properly structured. But, today, insurance companies have a better way to do this job by leveraging AI. Using AI to automate the process of regulatory change management by automatically identifying changes in regulatory requirements that apply to your organization and notifying the regulatory intelligence manager.

- Data-driven policies: Data-driven strategies can help insurance companies reap better profit margins. For example, consider the case of agriculture insurance. Insuring a farm need not be done based on a static insurance policy. Rather, creating a dynamic policy based on data points like the weather conditions in the region, climatic parameters, etc would give a better insight for the insurer on the potential insurance risks. Using an AI-based solution that can classify the clouds and predict their occurrence in a region can help insurance companies to better evaluate the risk associated with insuring companies that are affected by clouds.

For example, a solar farm that is built in a place that is cloudy throughout the year is obviously going to be at a loss. Ensuring this company would be a high risk for the insurer. Moreover, using such a solution, insurance companies can better evaluate the businesses that are affected by clouds before insuring them.

The future of AI in insurance

AI for insurance companies has the capacity to bring a lot of positive change. AI can help transform the image of the insurance industry: from slow and bureaucratic to fast and efficient. AI can deliver better experiences for customers by understanding their needs and providing personalized services, hence improving profits and reducing costs by automating processes. The more AI is used in insurance, the more expertise is achieved. If AI is leveraged properly, we will see flexible insurance based on the enormous data collected. Demand insurance, pay-as-you-go, and premiums that change according to health, accidents, etc will become commonplace, making the industry more customer-friendly and hence more alluring. Customer interaction can be made smoother and simpler, inviting more customers to take up insurances.

How to get started?

Once you have made up your mind and are ready to leverage AI for your insurance company, you might want to start out with a plan. Do a little research and figure out your weak areas. Develop a coherent plan on what areas you wish to optimize by the applications of AI in insurance. Choose the right partner in the AI industry who fits your needs and requirements. You can get technical support and advice from our team of experts here.

Once you implement AI in insurance, you need to wait and watch to reap the benefits of this technology!

[contact_sales title=”Need help developing your AI project?” desc=”Reach out to us today and get started!” btn_text=”Contact Us” url=”https://accubits.com/ai-development-company/”]