DeFi or Decentralized Finance is the latest hot trend in the fintech space and has caught the attention of several entrepreneurs, especially those involved in the BFSI sector. On preliminary research, you’ll see that DeFi is the technology used to enable financial services on a decentralized nature. Ruling out the middle men like banks and financial institutions from the equations and leveraging automation to execute direct financial transactions between the participants.

Isn’t this similar to what we all read about blockchain technology’s applications in the financial services industry?

Is DeFi just a new buzz name given to the same old use cases we read a lot? Or Is there something revolutionary and new about DeFi?

Let’s learn more about DeFi from the below sections:

- What is DeFi?

- Basic characteristics of a DeFi dApp

- Benefits of decentralized finance

- Why do we even need decentralized financial services?

- Use cases of DeFi

- Popular DeFi products

What is DeFi?

DeFi stands for “decentralized finance” and acts as a financial ecosystem that is built on top of blockchain technology. It is a collective term for services like investing, borrowing, lending, trading, and other financial services based on decentralized, non-custodial infrastructure.

It involves the use of decentralized networks and open source software to develop various financial services and products. The idea is to build and operate financial dApps on top of a transparent and trustless framework, such as permissionless blockchains and other peer-to-peer (P2P) protocols.

Between September 2017 and August 2020, the total value locked up in DeFi contracts has exploded from US$2.1 million to US$6.9 billion (£1.6 million to £5.3 billion). Since the beginning of August alone it has risen by US$2.9 billion.

Decentralized Finance can include digital assets, protocols, smart contracts, and dApps. DeFi products are well received in the market, the image below shows some of the very recent updates in the DeFi space.

DeFi provides a completely decentralized option for a trustless financial system. There are different types of lending and credit platforms within the DeFi space. These projects employ different strategies to allow users to borrow from and lend to each other with no central entity involved.

The main uses for DeFi include:

- Creating monetary banking services (e.g., issuance of stablecoins).

- Providing peer-to-peer or pooled lending and borrowing platforms.

- Enabling advanced financial instruments such as DEX, tokenization platforms, derivatives and predictions markets.

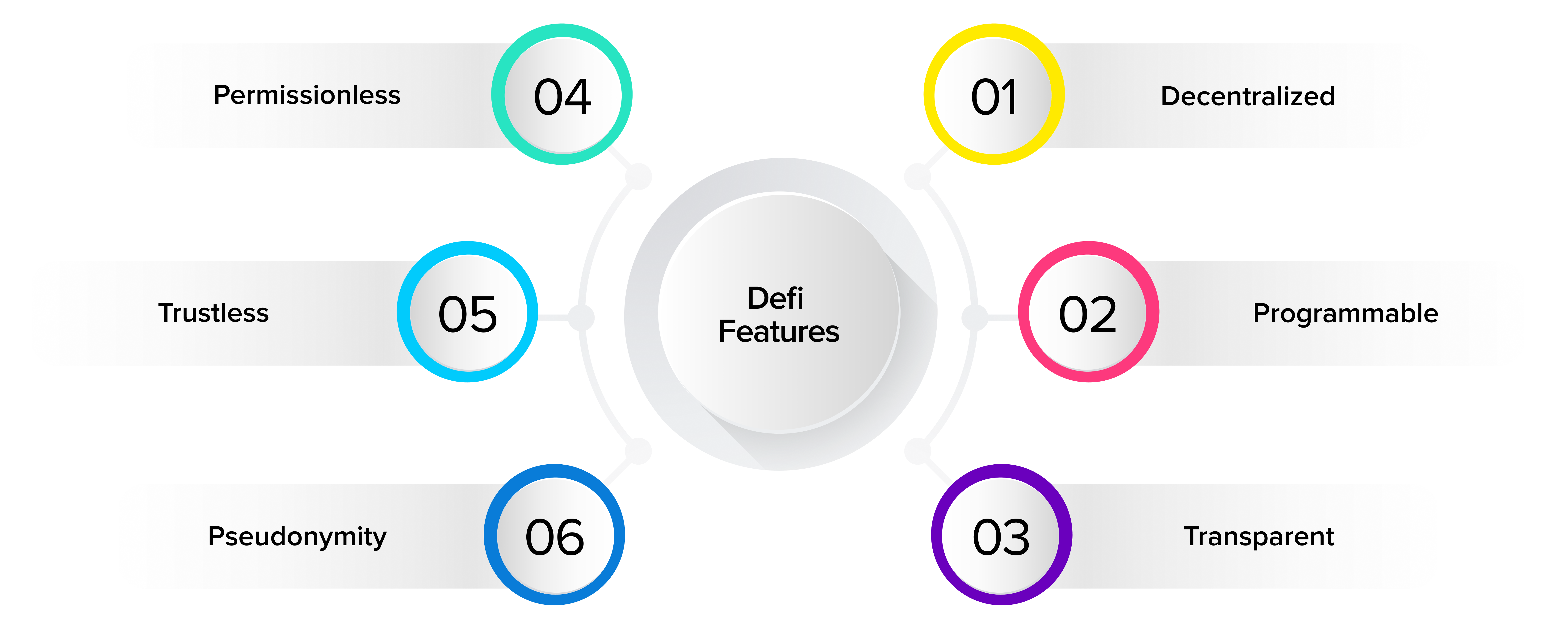

Basic characteristics of a DeFi dApp

The following are a few basic characteristics of a DeFi app. However, these are not strict defining factors for a DeFi dApp as many of the existing DeFi apps in the market do not all of there characteristics.

- The dApp offers a service/product available in legacy banking and financial services such as trading, lending, funds etc in a decentralized P2P channel.

- The user of the dApp needs to connects their crypto wallet to the decentralized blockchain network. For example, if its an ethereum based dApp, user need to connect their wallet to blockchain using metamask or other such services.

- The assets are 100% under self custody. There is no custodian to manage the assets of the user.

- All transactions, processes, workflows of the app are handled via smart contracts and a third-party involvement is not possible.

- No access restrictions. Anyone interested should be able to use the app with out any restrictions such as geographical, jurisdictional, minimum usage limits etc.

Let us have a look at some of the main points of difference that set DeFi dApps apart from traditional banking systems.

Business operations aren’t under the management of an institution and its employees. All the rules are written in code (or smart contracts). Once the smart contract is deployed to the blockchain, DeFi dApps can run themselves with little to no human intervention

- The code is completely transparent on the blockchain and can be audited by anyone. This creates a trustless system, since everyone is allowed to understand the contract’s functionality or find bugs. All transaction activity is also available for public viewing.

- It is a global system: Users have access to the same DeFi services and networks, irrespective of their location. The only requirement is a secure internet connection.

- They are completely permissionless in nature: Anyone can create DeFi apps, and anyone can use them. Users interact directly with the smart contracts from their crypto wallets.

- Guaranteed interoperability: New DeFi applications can be developed by blending other DeFi products. For example, stablecoins, decentralized exchanges, and prediction markets can be combined to form entirely new products.

Benefits of decentralized finance

DeFi is developed on top of a blockchain. This means that it inherits the security and transparency that comes with blockchain technology.

Its core benefits are-

- DeFi promotes autonomy. The money and assets that you own in a DeFi ecosystem are yours and yours alone. There is no centralized authority, such as a bank, with the ability to freeze your account, seize your assets, or block your transactions.

- Completely decentralized in nature. This allows censorship resistance and global participation irrespective of social status. It also eliminates the requirement for intermediaries or middlemen.

- Since it is built on top of a blockchain, it enables speedy and low-cost transactions, the immutability of the financial contracts, and contract automation.

- DeFi applications provide an extremely secure private key to its users. The user is in full control of the money without having to rely on a third party.

- Increased ecosystem transparency and thus price and market efficiency. Minimal principal-agent risks, as asymmetric information is non-existent and the personal interests are governed by a transparent protocol.

- Single points of failure are eliminated. The data is recorded on the blockchain and spread across thousands of nodes, making the shutdown of services nearly impossible.

[contact_sales title=”Need help with DeFi implementation?” desc=”Reach out to us today and get started!” btn_text=”Contact Us” url=”https://accubits.com/contact/”]

Why do we even need decentralized financial services?

People have used the barter system for exchanging goods and values since time immemorial. Around 600 B.C., they switched from the barter system to the concept of money. And by the 15th century, banking and financial systems evolved and expanded to a great extent. Over these years, several reforms have been made to banking systems and today we have a fairly good system.

Financial services have typically involved a centralized approach, it has central authorities that are responsible for issuing currency and facilitating trade. These authorities have the ultimate power to manage and regulate the flow and supply of currencies in the market. It’s all good. We are used to it. We’ve been running businesses, managing finances with this age old and proven method. But, the question is, is there room for improvement?

Financial system has undergone major changes from time to time. Are we on the cusp of the next major change in the financial system? Change is inevitable and it happens if a system is not as efficient or not serving the needs of the greater mass. So we need to take a look at the state of the existing systems. Are our current financial systems absolutely fail proof? Let’s consider a few examples.

Overseas Money Transfer

International payments tend to be a very laborious process. They take a lot of time and can be extremely risky as well. Additionally, the chances of hidden fees cropping up are very high. Businesses can incur flat fees on incoming wire transfers, which can be a $20–50 fee assessed on receiving the wire. On top of this, intermediary banks are sometimes in the middle of a transaction and charge their own additional wiring fee. These banks also charge a premium on foreign exchange, which is often a large margin above the mid-market exchange rate. These types of payments are also very susceptible to fraud. These limitations create several reservations around international payments.

The Great Recession

The recession of 2008 encompasses both the U.S. recession, officially lasting from December 2007 to June 2009, and the ensuing global recession in 2009. A great deal of damage was done to financial institutions all over the world due to excessive risk-taking by banks combined with the bursting of the United States housing bubble.

The economic crisis initially started in the U.S. but eventually spread to the rest of the world. This is because U.S. consumption accounted for more than a third of the growth in global consumption between 2000 and 2007 and the rest of the world depended on the U.S. consumer as a source of demand.

According to the Financial Crisis Inquiry Commission, the Great Recession was avoidable. Some of the key contributing factors that led to the crisis included the failure of the government to regulate the financial industry, extremely risky decisions taken by financial institutions, weak and fraudulent underwriting practices and overall, a faulty banking model.

The great recession clearly demonstrated the dangers associated with leaving a centralized authority in charge of financial systems. Humans can make mistakes and take unnecessary risks. The decision of a single entity can adversely affect the entire world.

What if central authorities make bad decisions while issuing currency? For example, Venezuela experienced severe currency instability due to the government’s inefficient monetary policies, which included printing huge amounts of money amid an oil price drop. This resulted in severe inflation exceeding 1,000,000% as per IMF data.

Clearly, there is room for improvements for the current financial systems. So, is that why we have blockchain based crypto currencies? – to solve these problems with the financial systems?

Bitcoin, along with other types of cryptocurrency have helped in solving this problem to a certain extent by facilitating secure peer-to-peer trading without the need for intermediaries like a bank for trade settlement. This gives users complete control over their assets. However, this is not a complete solution for the problems we discussed above. Although cryptocurrencies have decentralized currency issuing and storage, it has not decentralized the financial system as a whole. The major issues that stunt the growth of decentralization in the finance industry include-

- Although cryptocurrencies are decentralized, they are often accessible via centralized access points such as exchanges.

- Most of these crypto projects are managed through centralized companies that lack accountability or transparency.

A centralized system allows risk and vulnerabilities to accumulate in the centre of the system, which consequently endangers the system as a whole. In such a scenario, it is important to make our financial system more fair and transparent. The solution lies with decentralized finance, which can allow us to take control of our assets and our financial decisions.

[contact_sales title=”Need help with DeFi implementation?” desc=”Reach out to us today and get started!” btn_text=”Contact Us” url=”https://accubits.com/contact/”]

Use cases of DeFi

Let’s take a look at some of the most popular decentralized finance applications on the market

- Open Lending Platforms: Open lending platforms are one of the most popular use-cases for DeFi. These are typically simple decentralized applications (dApps) that allow you to lend and borrow your digital assets to other users in exchange for interest.

- Decentralized Exchanges: the well-known decentralized exchange apps are another common use case for DeFi. These are primarily cryptocurrency exchanges that do not need a central authority. More importantly, it allows users to transact directly with other peers while maintaining user access. As a result, it aids in the reduction of market manipulation, fraud, and hacking.

- Decentralized Insurance: DeFi is undoubtedly discussing the insurance industry as well. This sector deals with contract violations and fraudulent insurance claims due to a lack of proper management and protection.Furthermore, the process of filing an insurance claim takes a long time. As a result, a range of decentralized applications across this spectrum are using blockchain to secure and cover contracts while also assisting in the faster processing of insurance claims.

- Synthetic Asset Issuance: Synthetic asset issuance is basically the method of generating a digital commodity token that mimics the properties of something else, analogous to how a stablecoin exactly suits the value of the currency or asset to which it is pegged.For example, a synthetic asset can be made up of a certain percentage of fiat money and gold. Furthermore, this process aids in the absorption of any future price shocks. As a result, if gold prices fluctuate, fiat money can back it up and keep the end value stable.

- Staking: Staking is often one of the first ways for many digital asset holders to gain exposure to decentralized finance. This is the method of participating in the network governance of Proof-of-Stake (POS) blockchains by either delegating digital assets to a validator node or simply keeping these digital assets in a compatible wallet.

Popular DeFi products

Open Lending Protocols

This refers to s a digital money lending platform built on a blockchain. Similar to a bank, users deposit their money and earn interest, if someone else borrows their digital assets. However, smart contracts are used instead of third parties to dictate the loan terms. These contracts are also responsible for connecting lenders and borrowers, and distributing the interest. It offers several advantages over the traditional lending/crediting services –

- Integration with digital asset lending or borrowing.

- Collateralization of digital assets in case of defaulting on the loan.

- Instantaneous settlement of transactions and new secured lending methods.

- Standardization and interoperability which can also reduce costs with automation.

- No credit checks, meaning broader access to people that cannot tap into traditional services.

Examples for such protocols include Dharma and BlockFi. The latter allows users to borrow and lend digital assets but employs familiar credit models like credit checks and a company processing loan requests on the backend.

Stablecoins

Unlike other crypto coins which have a volatile value, stablecoins are blockchain-issued tokens designed to hold on to a specific value. A stablecoin can be pegged to a cryptocurrency, fiat money, or to exchange-traded commodities (such as precious metals or industrial metals).

Stablecoins can be primarily categorized into 3 types:

- Fiat-Collateralized: These coins store their value in fiat currencies like the US dollar or Euro and are usually supposed to be redeemable at a 1:1 ratio with the pegged currency.

- Crypto-collateralized: These decentralized stablecoins are backed by crypto assets as collateral. They rely on trustless issuance and maintain their 1:1 peg against assets through various methods including over-collateralization and incentives.

- Non-Collateralized: These types of stablecoins are neither centralized nor over-collateralized with crypto assets. Based on an algorithm, the system supplies more tokens with increased demand while the price of each token is lowered and vice versa in order to maintain a stable peg.

Exchanges and Open Marketplaces

Decentralized exchanges are very different from centralized ones like Coinbase. They involve peer-to-peer transactions of digital assets between two parties on the blockchain with no third-parties involved. The advantage of this approach is that there are no sign-ups, no identity verification, or any withdrawal fees. IDEX is the most popular DEX – a dapp on Ethereum blockchain. Other DEXs include Binance DEX, Radar Relay, and EtherDelta.

Other types of open marketplaces focus on non-fungible tokens (NFTs) exchange. These tokens are often referred to as crypto-collectibles. OpenSea and Rarebits are two such platforms that help the exploration, discovery and buying or selling of such crypto-assets. There are also some marketplaces like District0X which allows for the creation of marketplaces to vote on governance procedures.

DeFi boosts the functionality and reach of money, while providing a financial system that is more open and liberalised than ever before. The DeFi market is quite small in relation to traditional finance, but it is expanding at rapid rates. This creates much hope for a financial revolution that supports decentralization and transparency. It takes us one step closer to democratizing the global economy, making money and payments universally accessible to everyone.

To know how to launch a DeFi project, refer this article – How to launch a DeFi project

[contact_sales title=”Need help with DeFi implementation?” desc=”Reach out to us today and get started!” btn_text=”Contact Us” url=”https://accubits.com/contact/”]