We believe in AI and every day we innovate to make it better than yesterday. We believe in helping others to benefit from the wonders of AI and also in extending a hand to guide them to step their journey to adapt with future.

Even though the government is skeptical about cryptocurrency, it did not fail to realize the immense potential of blockchain technology. But the finance ministry openly revealed that it does not support private cryptocurrencies. Can there be a currency that has the convenience of crypto but is much safer and less volatile? That is exactly what a Digital Rupee, or the Central Bank Digital Currency (CBDC) of India, is. Regulated by the RBI, the digital currency will be used to buy goods and services in both retail and wholesale. The government rolled out the first phase of pilot tests with the wholesale sector. The next phase of the same will take place in the retail sector.

Digital Rupee is the digital form of Indian currency introduced by the Union Government of India in the 2022 budget. It significantly boosts the digital economy and improves the convenience of new technologies, such as the blockchain. The Finance Bill of India proposed that the Central Bank Digital Currency (CBDC) “should also be regarded as bank notes.” In short, digital currency is the Indian currency in all aspects but in no form because it exists digitally.

In 2020, the Supreme Court of India released the ban on cryptocurrencies set by the RBI. In 2022, the Government of India distinctly said in the Union budget of 2022-23 that the transfer of any unregulated digital currency/cryptocurrency asset will be under a tax deduction of 30%. Being the 7th highest crypto-holding country in the world, at least 7% of the Indian population invests in the same. The honorable finance minister of India, Nirmala Sitaraman, said,

“Introducing Digital Rupee, using blockchain and other technologies, to be issued by the Reserve Bank of India starting 2022-23.”

With the digital form of the rupee in place, India will extensively use the blockchain for seamless transactions, but the entity will be centralized in all its meaning. Roughly 40-50% of the Indian population performs digital transactions daily. Releasing the digital rupee to be used by the general public will only improve technical literacy in the country. It will force service providers to bring several off-grid areas in the country to come on-grid.

Digital currency improves scalability, liquidity, faster settlement, and acceptance with the privilege of staying anonymous in transactions. Unlike physical cash, payments done using CBDC are completely traceable.

Reach out to us today to discuss your project

Initiating a digital currency transaction through UPI instead of a bank account is like handing the cash directly to the recipient without going through interbank settlements. So if a person had to send money to someone in America in digital dollars, they could send it as Indian digital currency after converting it in real-time without the involvement of any intermediary. The RBI’s website also says that the digital currency will become a complex financial instrument based on its design.

On November 1, 2022, the Indian government rolled out the pilot test of the digital form of the rupee with the wholesale sector. It involved 9 selectively chosen banks to transact 50 government bond transactions worth about Rs 275 crore. State Bank of India, Bank of Baroda, Union Bank of India, HDFC Bank, ICICI Bank, and Kotak Mahindra Bank were a few among the chosen banks. The first pilot went by smoothly, and the pilot test in the retail sector is expected to take place in mid-November of the same year. The pilot tests are conducted in select locations with closed groups of customers and merchants.

The introduction of the digital form of the rupee in India is aimed at lessening the usage of currency notes. The RBI also aims to reduce the cost of printing and logistics of currency/bank notes along with the tedious cycle of circulation.

Truthfully, we can buy everything a digital currency can buy using traditional paper money. Then, how does it compare to cash in the nation’s economy?

A digital currency has properties similar to physical cash or notes. Similar to traditional cash, the transaction involving a digital rupee only happens in its digital form. So you now have multiple options of money available based on your convenience and feasibility.

Numerous interconnecting servers and online payment methods make data recording and its release much more feasible. This method is similar to the HTTP method used in web servers. Also, this method does not require the involvement of all servers for each transaction. Thus, faster transactions and a more transparent approach than the traditional system are similar to the working of blockchain-based decentralized finance ecosystems.

A single user could connect to the required ones without having several intermediaries, and these online forms of processing would not disrupt transactions. Following the drill of the peer-to-peer system of the blockchain, buyers and sellers can connect, surpassing intermediaries.

Digital currencies and crypto coins are gaining acceptance as genuine payment methods in the financial marketplace. They can lead to Innovative technologies that work using digital currencies. For example, the concept of blockchain-based money has already led to developments like swaps, derivatives, loans, and other investments.

The asset ledgers function here in the public-forum mode. Thus it is evenly distributed throughout the networking platforms. It is also possible to share this asset ledger with other private or semi-public groups.

The public will benefit from the continued development of new applications and other technological facilities, providing greater security and simpler modes of money transaction and savings plans. For blockchains, the APIs will have additional innovations on the list.

We can help you out!

The software’s core is a public model that allows transactions to be more visible, despite being digital. This open banking stage will allow for more enhancements to pre-existing software.

The anonymity of user-initiated transactions is fully protected. It means that the data is not accessible to third parties. The public’s account tracks are nearly untraceable. The rebranding of any feature or model of the digital currency will not affect its efficiency or operating system.

In the case of digital currency, energy usage or redemption is quite low. Furthermore, because the entry barriers are minimal, digital currency is useful for carrying out smaller transactions.

If digital currency is the same as regular money and serves the same purpose, how is it different? Or how do you tell which rupee is which?

There has been enough confusion about the operational and functional side of a CBDC. Another doubt arises when people think about how the CBDC differs from the regular rupee in a bank account used to transact through the Unified Payment Interface. Let’s turn to The Bahamas for some answers.

The Bahamas launched its CBDC called the Sand Dollar in October 2020. Digital wallets or e-wallets hold the digital currency Sand Dollars. So users can access it via a physical payment card or a mobile app. Users send proprietary applications, and authorized agents enroll them to be eligible to use the digital currency. A tier system serves as the basis for an e-wallet. The basic one, tier-Ihas a holding limit of $500 and a transaction limit of $1500. The basic level does not offer the provision to connect bank accounts. It can’t be linked unless verified using a suitable government ID.

Tier-II e-wallets, on the other hand, can be linked to bank accounts. They have a holding limit of $8000 and a transaction limit of $10000. They do require the users to submit government IDs. The Bahamian and Sand Dollars are different, except users can move them from an e-wallet to a bank account. The only catch is that users must give up the anonymity privilege to go up to higher tiers and link bank accounts. RBI’s balance sheet shows that digital and physical currencies are fungible and treated equally.

If you did not quite catch it yet, the major difference is that digital currencies will exist on a blockchain. Existing digital currencies in countries such as the Bahamas even allow anonymous transactions like cryptocurrencies. UPI serves as a medium for transacting physical money through the digital space.

The CBDC issued by the Reserve Bank of India helps control the monetary policy and provides relief measures on time in scenarios like the pandemic. One of the most controversial duties in finance is tax collection, which can be done efficiently with digital currency. The CBDC also makes the financial system more inclusive, as users can make direct transfers straight to people’s phones at low costs.

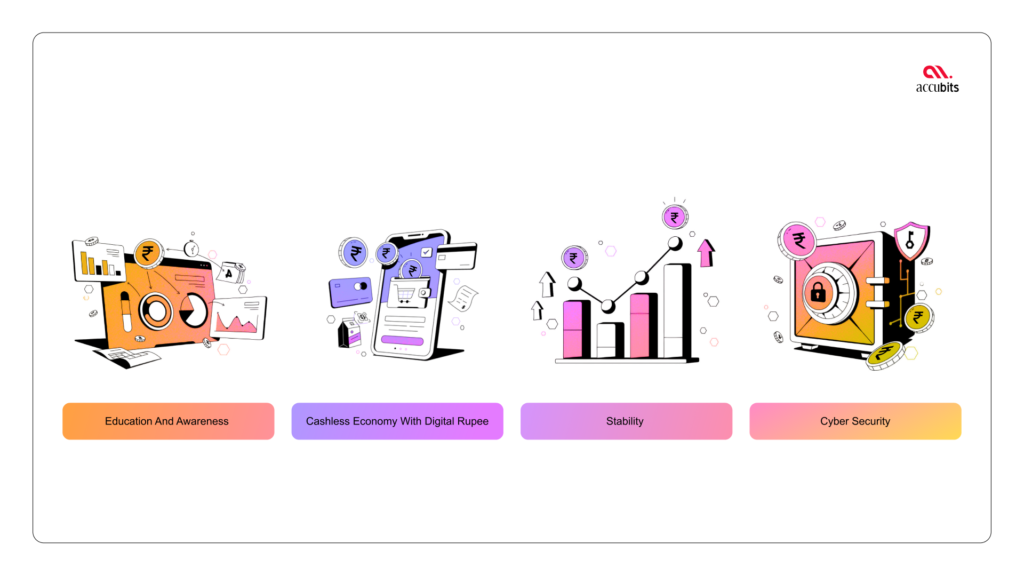

The CBDC will be a first step towards educating more and more people about digital transactions to promote a stable cashless economy. The secure nature of the public ledger, which is also the reason for its stardom, can help reduce financial crimes. Here are some other benefits the government will reap because of digital money.

The global interest in digital currency has been surging. According to research by Chain analysis India is one of the countries with the fastest crypto adoption by individual investors. The exposure indicates more consumer adoption. Thus introducing a digital currency automatically educates and spreads awareness about the digitization of retail and other financial markets.

Digital currency eliminates the need to carry large amounts of cash between individuals. With the onset of the CBDC, the transactions would be less complicated, easily monitored, and transparent.

The crypto market witnessed high volatility in its initial years, and today several digital currencies and cryptocurrencies remain unpredictable. But India’s digital currency, as the real Indian money, will not have stability issues. Seeing the growing adoption of blockchain-based solutions, stable digital money with the convenience of blockchain must boost people’s confidence in payments.

India had 11,58,208 cyber security incidents in 2020-21. Cyber security attacks increased to 12,13,784 by October 2021.

The launch of digital rupee can resolve the threat of cyber attacks by 60 – 70%.

Every blockchain-based transaction in a private or public blockchain network has a unique digital signature or time stamp to keep them secure. Also, this allows organizations to trace transactions to a specific period and discover the corresponding person on the blockchain using their public address. Moreover, the audit capabilities of the blockchain ensure that each transaction in the network is secure and transparent.

The digital currency of India supports a wide array of use cases. These use cases range from faster lending and payments across financial institutions to programmed payment systems for subsidies. As such, it is a major boost for the cashless economy that the country aims to reach via increasing cashless payments. As the transactions using digital currency increase, it could also benefit things like international payments and interoperability with a remittance system that is much faster.

Schedule a no-obligation consultation call now!